Hydropower’s Role in a Net Zero Europe

Master the Moment and Reach Your Peak with Defoes

“Defoes looks past Europe’s solar and wind headlines to show how legacy dams and new pumped‑storage schemes are quietly becoming the flexible backbone that keeps a net‑zero power system investable.”

Hydropower is the oldest of Europe’s renewables, but in a net‑zero system it is also one of the most modern tools the continent has. European hydropower generation rebounded strongly in 2024, reaching its highest level in a decade at about 680 TWh as rainfall recovered and systems leaned more heavily on renewables. At the same time, total installed hydropower capacity in Europe climbed to roughly 262.7 GW, underlining that water remains a core pillar of the continent’s electricity mix even as solar and wind expand. From Defoes’ standpoint, the bullish stance is straightforward: in a system dominated by variable renewables, hydropower’s value is shifting from “just another renewable” to the backbone of flexibility, storage and system resilience.

From baseload workhorse to flexibility engine

Hydropower is already the second‑largest renewable power source in the EU, generating around 355 TWh annually in recent years, but its strategic importance goes well beyond raw output. Reservoir and run‑of‑river plants can ramp production up and down quickly, filling gaps when wind or solar fall short and providing critical services such as frequency control, reserve provision and black‑start capability. European hydropower position papers and white papers consistently describe the technology as a “key pillar” of flexibility and storage, essential to operating a safe and secure power system dominated by variable renewables.

The European Commission and industry bodies are beginning to codify this role. Hydropower has been formally recognised as a key technology in the EU’s Net‑Zero Industry Act, with stakeholders arguing that it should be explicitly listed as a “strategic net‑zero technology” due to its unique contribution to stability and security. That recognition reflects decades of performance: for much of Europe, hydropower has been the bedrock of renewable generation and remains one of the main ways systems cope with sudden changes in supply and demand.

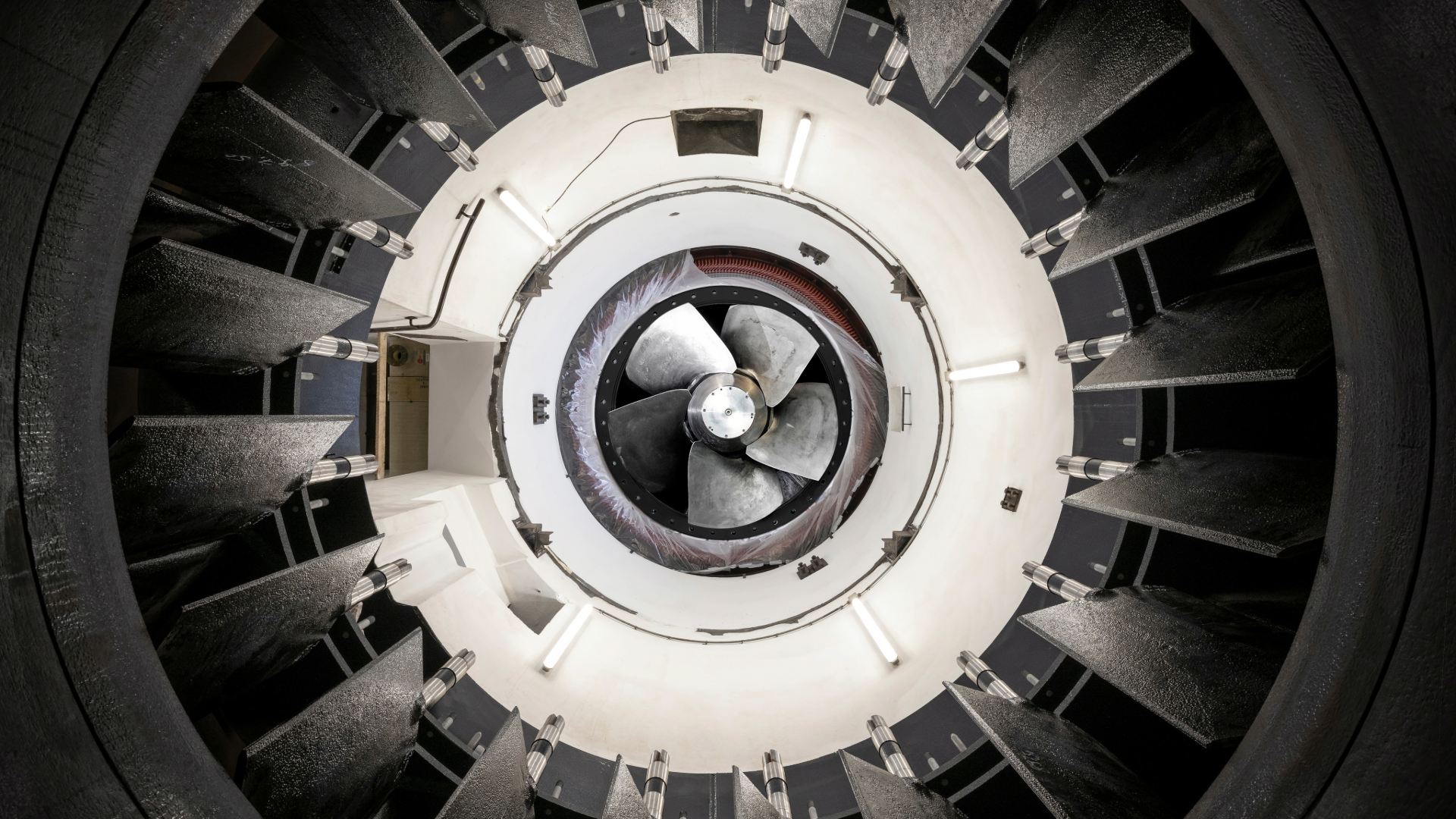

Pumped storage: Europe’s de‑facto long‑duration battery

If conventional hydropower provides flexible generation, pumped‑storage hydropower (PSH) provides storage at scale. PSH already accounts for over 90% of the EU’s existing electricity‑storage capacity, making it the only mature technology able to store energy from minutes to days at the gigawatt scale. EU and industry analyses stress that PSH absorbs excess wind and solar output during periods of high generation, reduces curtailment, and then releases energy when demand and prices are higher. This capability is central in decarbonisation scenarios: modelling of future European systems finds that storage, especially long‑duration storage, is indispensable to meeting net‑zero targets while keeping reliability within acceptable bounds.

The pipeline is expanding. The 2025 World Hydropower Outlook reports that Europe is seeing growing interest in new PSH projects as policy momentum builds, with hydropower additions globally reaching 24.6 GW in 2024, of which 8.4 GW came from pumped storage. Industry and utility groups such as the International Hydropower Association and Eurelectric have launched joint calls to accelerate PSH deployment, framing it as “essential to building resilient, net‑zero electricity systems”.

Hydropower in a net‑zero portfolio: why the bullish case holds

Hydropower also brings advantages beyond electrons. European hydropower advocates highlight that the technology is built on largely domestic value chains and is comparatively autonomous from critical raw materials that constrain some other low‑carbon technologies. Multipurpose reservoirs can support not only power generation, but also flood management, drought mitigation, irrigation, navigation and ecosystem services, increasing their social and political value in a changing climate. In net‑zero planning, these co‑benefits strengthen the case for upgrading and repowering existing plants and for adding PSH capacity where environmental and social constraints can be credibly managed.

There are material risks and constraints: climate change can affect hydrology; environmental concerns limit new large‑dam projects; and market frameworks do not always adequately reward flexibility and storage services. Yet the direction of policy and system design is increasingly aligned with hydropower’s strengths. The EU’s recognition of hydropower under the Net‑Zero Industry Act, the rebound in European hydropower output, and the renewed push for pumped storage all point to an asset class moving from legacy status to strategic infrastructure for a net‑zero grid.

From a Defoes perspective, the stance is that hydropower’s role in a net‑zero Europe is not optional or nostalgic; it is structural. In a system where solar and wind provide ever‑cheaper energy, water‑based assets — reservoirs, run‑of‑river plants and pumped‑storage schemes — will increasingly provide the flexibility, inertia and long‑duration storage that keep those variable resources bankable and reliable. The analytical task for investors is to understand where policy, regulation and hydrology are converging to turn that system value into stable, long‑dated cash flows — and where gaps in market design still need to be closed before hydropower’s full potential in Europe’s net‑zero pathway can be realised.